Q016

Why plan anyway?

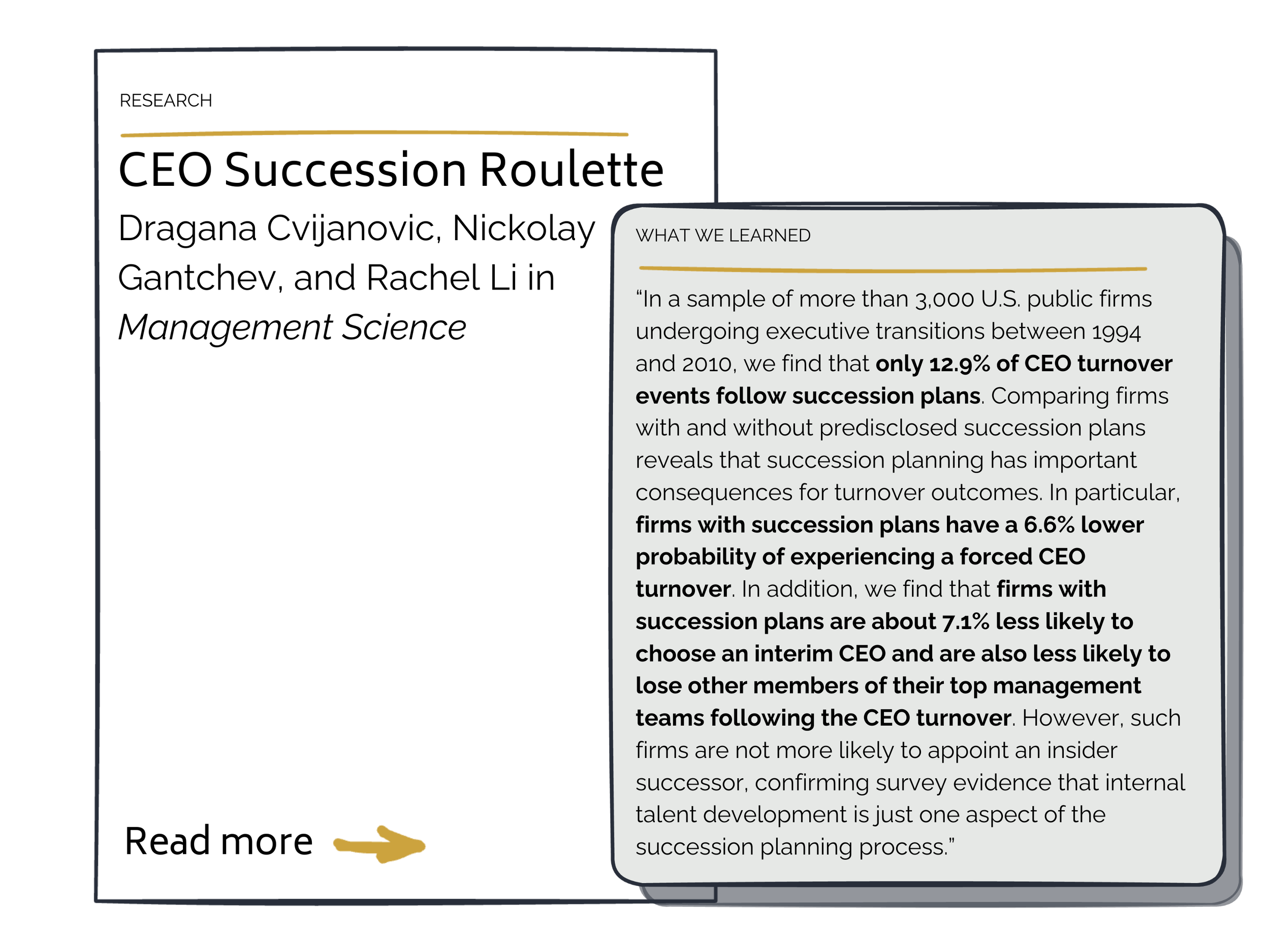

our take .

We once wrote in an essay on why plans may not work out: “For us, planning with uncertainty is figuring out how to build the only sure thing – that things won’t go according to plan – into the plan. We think the best way to do this is to approach each situation with high intellectual honesty, high humility, high optimism, and a growth mindset. It’s a posture, over a plan, that embraces learning, adaptation, and iteration.”

Much of this series has emphasized the value of being proactive in succession planning. But it’s equally important to recognize a hard truth: very few people will voluntarily initiate the process – and the more closely held the business, the more that holds true. After all, who is going to walk into the owner’s office and say: “So, when are you retiring?” In most cases, as long as the owner wants to hold on and is healthy, he or she can.

Warren Buffett’s announcement at the 2025 Berkshire Hathaway Annual Meeting earlier this month underscored this reality. More than four hours into the meeting, he began:

“Tomorrow we’re having a board meeting of Berkshire. We have 11 directors. Two of the directors, who are my children, Howie and Susie, know of what I’m going to talk about there. The rest of them this will come as news to. But I think the time has arrived where Greg [Abel] should become the Chief Executive Officer of the company at year end. And I want to spring that on the directors effectively and give… that’s my recommendation. Let them have the time to think about what questions or what structures they want…”

Can you imagine “springing” that announcement on a board in front of nearly 20,000 people? Berkshire after Buffett has been a source of speculation for years. After all, Mr. Buffett will celebrate his 95th birthday this summer (what a run!)! Yet he individually made the call, with the support of his family, to set the succession plan in motion.

The family awareness of his decision is also significant. Mr. Buffett had discussed what is best for both the organization and for him individually with those who have aligned interests in both.

He went on to promote why Mr. Abel is his recommendation and to offer several forms of his transitional and ongoing support. Mr. Buffett had referenced Mr. Abel several times over the years as his likely successor, dating back to 2021. His growing responsibilities were intentionally noted in each annual update, but a timeline was never discussed — until Mr. Buffett decided to “spring.”

The takeaway: If you plan, you are prepared to make a call. And someone has to make that call.

on paper.

character to consider: Kevin Planck

There and Back Again: A CEO’s Tale

There are a lot of ways to try to get a transition to stick, but when the news is rife with stories of high-profile founders and CEOs who leave and, seemingly inevitably, come back to take the reins again when things go sideways (Howard Schultz, Bob Iger, Steve Jobs…), planning for a succession can feel like a fool’s errand. Same goes for Under Armour: Kevin Plank, who founded the company in 1996, stepped down as CEO in 2019. His successor, Patrik Frisk, was tasked with stabilizing the company amid increasing competition and financial challenges. In 2023, Stephanie Linnartz took over as CEO, bringing experience from the hospitality industry but lacked a deep background in retail or apparel. Her tenure lasted less than a year before Plank resumed the role in 2024, citing a need to leverage his understanding of the brand during a critical juncture. (His return led to a 10% dip in stock prices.)

Founder-Dependent

Over time, founder-led companies often veer into founder-reliant companies without careful planning. Even after stepping down as CEO, Plank remained as Executive Chairman and brand visionary, keeping the company, despite transitions in leadership, closely tied to his vision, style, and influence. His continued presence in key decision-making roles made it difficult for successors to lead independently. Planning, even against headwinds, signals a willingness to shift, combatting innovation stagnation, stakeholder skepticism, and talent retention issues.

Dependent Founder

But it’s also chicken-egg. Plank built Under Armour from scratch and long occupied a position as face of the brand. Charismatic leadership + personal story as a former athlete = difficulties for successors in establishing their own authority. But it also = difficulties for outgoing leaders in really letting go. From The Hero’s Farewell: “Many top corporate warriors do not quietly recede. Before their light is extinguished, it flares up in a final flash of glory. The corporate general leaves office reluctantly…[and their] desire to continue to direct their firms’ activities makes it difficult for them to depart quietly.” And, it means they often find themselves back at the helm in moments of crisis – a result that was almost certainly not part of the plan.

Works consulted:

Kevin Plank Broke Under Armour. Can He Fix It?

Under Armour Stock Sank on CEO's Return—How Have Other CEO Comebacks Affected Shares?

Under Armour founder Kevin Plank returns as CEO

Kevin Plank can’t let go of Under Armour. Is that hampering a turnaround?

We welcome your questions, feedback, and suggestions as series installments are released. Our emails are:

Subscribe to receive new installments in the series.

The information, opinions, and views presented in this publication are provided solely for general informational and educational purposes. They should not be interpreted or considered as legal, tax, financial, or other forms of professional advice. All information, opinions, and views expressed herein are of a general nature and have not been tailored to address the specific circumstances or needs of any individual or entity. As such, they do not constitute a comprehensive or complete statement of the matters discussed. Readers should consult with their own legal, tax, financial, or other professional advisors regarding the applicability of this information to their own circumstances.

This publication may include links to third-party websites and provide access to other third-party content, such as articles, news reports, company information, or other materials (collectively, “Third-Party Content”). These links and resources are provided solely for your convenience and general informational purposes. Permanent Equity Management, LLC (“Permanent Equity”) does not endorse, approve, certify, or guarantee the accuracy, completeness, or timeliness of any third-party websites or Third-Party Content, nor does Permanent Equity imply any affiliation, partnership, or endorsement between us and the owners/operators of any third-party websites or the providers/creators of any Third-Party Content. Permanent Equity has no control over third-party websites or their content and disclaims any responsibility for their accuracy, security, privacy policies, or the quality of any products or services offered through them. Accessing third-party websites or relying on Third-Party Content is done entirely at your own risk. Permanent Equity is not liable for any damages, losses, or liabilities arising from your use of, access to, or reliance on third-party websites or any Third-Party Content. Any transactions, decisions, or actions made based on third-party websites or Third-Party Content are solely between you and the respective third party.

The information provided in this publication does not constitute investment advice, nor does it represent an offer to sell or solicit the purchase of interests in Permanent Equity or any private fund it advises. It is not intended for marketing purposes to existing or prospective investors in any jurisdiction and may be subject to correction, modification, or supplementation without prior notice. Permanent Equity provides investment advisory services only to the privately offered funds it advises and does not solicit or make its services available to the public or other advisory clients.