Real Returns

Our CEO Brent sent out his annual letter earlier this month, which included musings on AI, the role of a CEO, board members, selling, and more. One of the most interesting sections, however, was his discussion of fees and performance in private equity. He cites several studies to conclude that “in traditional private equity structures, the GP is both taking a significant portion of the total return and doing so independent of performance.”

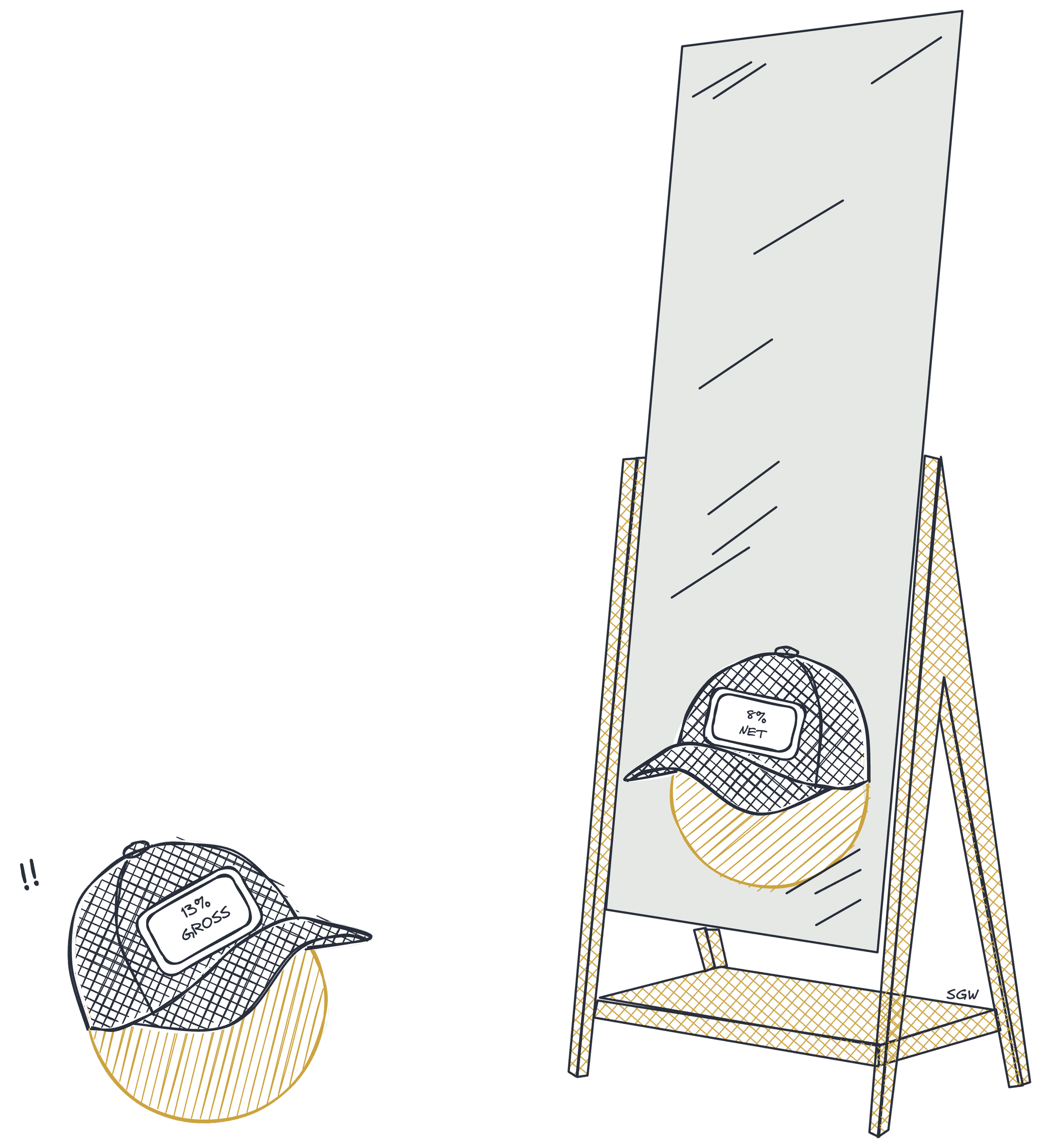

When performance is good, this maybe isn’t a big deal. After all, no one is really going to grouse about the difference between a 30% gross and 25% net return. But if 13% gross becomes 8% net because of fixed fee drag, well, your investors will probably let you know that they would have been better off buying an index fund.

So how good are private equity returns really? Historically, they’ve been good. But historically money was cheap and there wasn’t as much competition. So it’s a good question if private equity returns going forward – with more expensive capital and more people bidding for deals – will enable the industry to continue to justify its high fees.

Two things are happening right now that suggest they may not. First, midlevel employees are reportedly leaving large private equity firms “due to uncertainty about receiving carried interest.” Second, large private equity firms are selling assets to themselves via continuation vehicles at record rates.

Taken together, those two phenomena suggest something subtle but important: recent real returns are likely materially lower than what’s being reported in spreadsheets. Further, they’re not likely to improve, at least in the near term. After all, if the people who would know don’t think there are performance fees to be had, and the firms themselves are reluctant to put verifiable numbers on the scoreboard, that probably tells you all you need to know.

– Tim

Sign up below to get Unqualified Opinions in your inbox.

The information, opinions, and views presented in this publication are provided solely for general informational and educational purposes. They are of a general nature, have not been tailored to the specific circumstances of any individual or entity, and do not constitute a comprehensive statement of the matters discussed. This material should not be interpreted or relied upon as investment, legal, tax, accounting, regulatory, or other professional advice, and nothing in this publication is intended to be or should be construed as such. You should obtain advice from your own professional advisors regarding the applicability of the information to your particular circumstances.

The views and analyses expressed are those of the author and do not necessarily represent or reflect the views, opinions, policies, or positions of Permanent Equity Management, LLC, its officers, directors, employees, affiliates, or portfolio companies, or of any person or entity with whom the author may be affiliated. Permanent Equity Management, LLC makes no representation or warranty, express or implied, as to the accuracy, completeness, timeliness, or suitability of the information contained herein and expressly disclaims any liability for errors or omissions.

This publication is not, and should not be construed as, an offer to sell, a solicitation of an offer to buy, or a recommendation of any security, financial instrument, or other product. It does not form the basis of any contract and does not create a fiduciary, advisory, or client relationship with Permanent Equity Management, LLC. Any examples or references to third-party content are for illustrative purposes only and do not constitute an endorsement. Permanent Equity Management, LLC is not responsible for the availability, accuracy, or content of third-party materials. Past performance is not indicative of future results. Any forward-looking statements are inherently uncertain and subject to change.